The Bullrun That Never Came for Altcoins

What Can We Learn From This Cycle?

The 2024 crypto bullrun has been far from what many expected. Instead of a rising tide that lifted all boats, it felt more like a narrow river that only carried a few forward, while most were left behind. Investors who came into this cycle with heavy altcoin allocations found it especially difficult, as the altcoin rally they were hoping for never truly happened.

At the center of this cycle’s story is Bitcoin. From its bottom around $15,000 in late 2022, Bitcoin has climbed by roughly 600% as of April 28, 2025. In stark contrast, Ethereum — often seen as the leading indicator for altcoins — bottomed near $900 and, despite briefly reaching $4,000, has only managed around a 100% gain from its lows. This divergence between Bitcoin and Ethereum captures the broader theme of the cycle: Bitcoin thrived, while altcoins largely lagged behind.

The ETH/BTC chart tells the story even more clearly. Throughout this bullrun, Ethereum has consistently lost ground against Bitcoin, setting a difficult backdrop for the entire altcoin market. Historically, when Ethereum underperforms relatively to Bitcoin, it signals weakness across the broader altcoin space. Altcoins bled steadily against Bitcoin, with few exceptions. Some alts, like SOL, managed to outperform Bitcoin for a period — notably during late 2023 to early 2024 — but these moments were rare and short-lived compared to the broader trend of altcoin weakness.

Another clear sign of how different this cycle has been is seen in TOTAL2, the total crypto market cap excluding Bitcoin. As of now, it still hasn’t been able to break past its previous all-time high of $1.71 trillion from 2021 bullrun. Even as Bitcoin has pushed into new highs, the altcoin market has struggled to catch up. Rather than new capital consistently fowing into the space, we’ve mostly seen existing capital rotating from one narrative to the next — from VC-backed projects, to memecoins, to AI plays, to hyperliquid trading ecosystems, and more recently, into BSC-based tokens — without any theme being able to sustain momentum for long.

This lack of broad participation is also evident in the Social Metric Risk Indicator, a metric developed by Benjamin Cowen and published on IntoTheCryptoverse, which tracks market hype through indicators such as YouTube subscriber growth, video views, and engagement from key Crypto Twitter (CT) accounts, including influencers and exchange handles. Throughout this cycle, the indicator never reached an overheated state — a stark contrast to previous bull runs. A likely explanation is that Bitcoin, rather than altcoins, led the rally. Retail investors — typically drawn to altcoins for their perceived explosive upside — often view Bitcoin as “too expensive” or offering limited gains. Without strong, sustained altcoin performance to ignite widespread FOMO, the market never reached the kind of euphoric, retail-driven peak that usually characterizes a full-blown crypto bull market.

There are several key factors that set this bullrun apart from previous cycles, each contributing to the unusually narrow market performance we've seen so far.

Oversupply of Tokens

One of the major reasons this bullrun feels so different lies in the sheer number of tokens that exist today. As of April 2025, there are over 37 million tokens in the crypto space— a staggering jump from fewer than 3,000 during the 2017–2018 cycle, and less than 500 back in 2013–2014. With token creation now easier than ever, thanks to Solana, Base, and Binance Smart Chain, developers can launch a token in minutes, often without strong long-term purpose. In fact, Solana alone accounts for around 70% of total token issuance, driven in part by memecoin platforms like pump.fun.

This explosion in token supply has created a market that’s extremely fragmented. Liquidity— which was once able to lift a broad range of assets during previous cycles — is now spread thin across millions of tokens, the vast majority of which are low-quality or inactive. While not all of these tokens are active or significant, their sheer number makes it difficult for capital to concentrate.

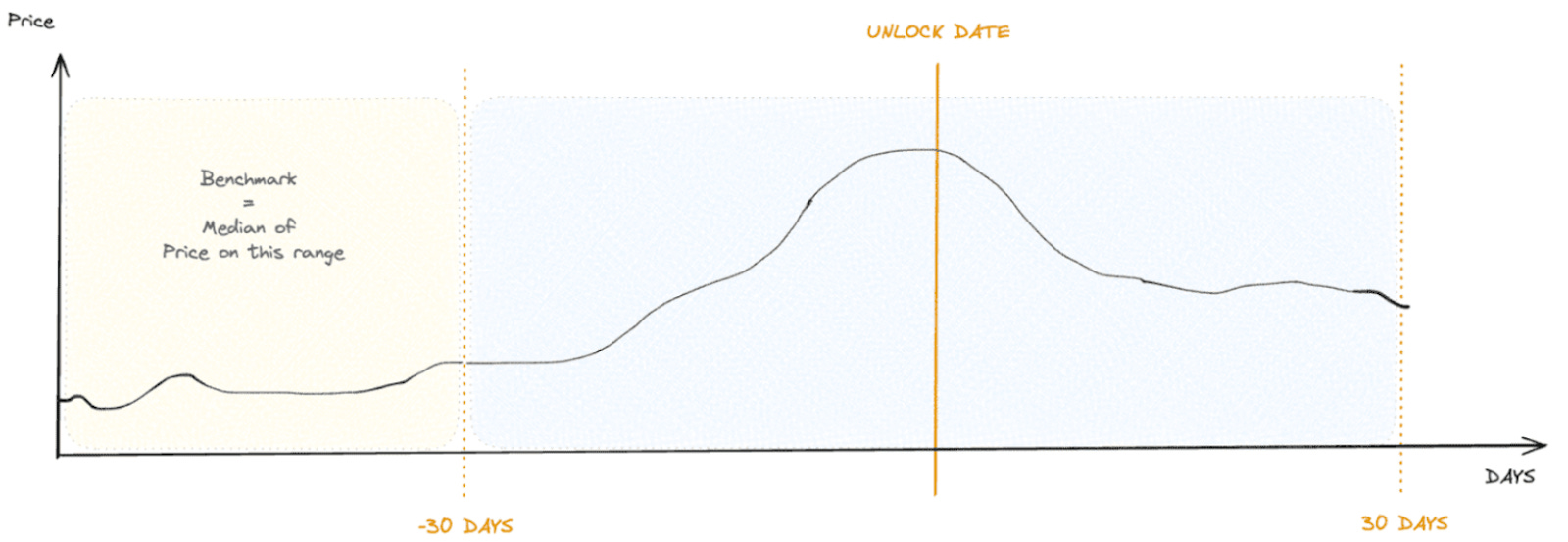

On top of that, there’s another structural supply issue: token unlocks. Every week, over $600 million worth of tokens are unlocked, flooding the market with new supply. Data shows that 90% of these unlocks create negative price pressure, with impacts often beginning 30 days before the unlock event. The larger the unlock, the more severe the price drop—team unlocks in particular can lead to crashes of -25%, while investor unlocks tend to be less disruptive due to smarter hedging strategies. Combined, the oversupply of tokens and the steady wave of unlocks have made it harder for individual assets to gain traction, further contributing to the different feel of this current cycle.

Bullrun Without QE

Another key factor that sets this bullrun apart from the past is the absence of supportive monetary policy. In previous cycle, especially the explosive 2020-2021 bullrun, market had the powerful tailwind of Quantitative Easing (QE): a macroeconomic policy where central banks inject liquidity into the system by buying assets like government bonds. This influx of liquidity doesn’t just stimulate traditional markets, it often finds its way into risk-on assets like crypto.

To visualize this, charts of global liquidity often shade QE periods in blue and QT periods in red. The last major QE began on March 15 2020, when the Federal Reserve launched its fourth round of QE since the 2008 financial crisis. In the response to the COVID-19 pandemic and the collapse of financial markets, the Fed committed to $700 billion in new asset purchases—and by mid-2022, this had added over $2 trillion in assets to its balance sheet. This massive influx of liquidity helped spark one of the most aggressive bullruns in crypto history, with TOTAL2 soaring more than 40x from its March 2020 low to its November 2021 peak.

However, QE officially ended in 2022, as inflation surged to multi-decade highs. The Fed and other central banks pivoted into Quantitative Tightening (QT)—the deliberate reduction of balance sheets and tightening of monetary conditions. We’ve been in this red-shaded QT era ever since. In a QT environment, liquidity is not just scarce, it’s actively being withdrawn. Combine this with the current state of the crypto market, where over 37 million tokens compete for attention and capital, and the result is a market where broad-based rallies are far less likely. This is why the era of “everything pumps” is much harder to replicate. Instead of riding a rising tide, investors now navigate a landscape of tight liquidity, saturated supply, and rapidly shifting narratives.

This Bullrun Is Institution-Driven

One of the most notable differences in this cycle is the clear dominance of institutional capital, rather than a wave of retail-driven enthusiasm. This shift in market structure is reflected in several key indicators that suggest institutions are playing the lead role this time.

One such signal comes from on-chain Bitcoin metrics, particularly the Short-Term Holder (STH) supply. In previous cycles, sharp rises in STH supply—held by newer entrants—reflected strong inflows from retail investors during peak hype phases. These phases often coincided with widespread distribution: long-term holders selling into retail FOMO. However, in the current cycle, STH supply hasn’t spiked in the same way, suggesting fewer new retail participants. This has contributed to a more gradual and less aggressive distribution process compared to past cycles.

What we’ve seen instead is a surge in institutional participation, primarily driven by the arrival of spot Bitcoin ETFs. As of April 30, 2025 , the total AUM in Bitcoin ETFs has reached $112 billion. In stark contrast, Ethereum ETFs only manage $9 billion, underscoring institutional preference for Bitcoin over alts.

Further evidence lies in inflow records. Bitcoin ETFs saw $6.61 billion in net inflows in November 2024 alone, marking the strongest monthly performance to date. By comparison, Ethereum ETFs peaked at just $2.05 billion in inflows during December 2024. This massive divergence reflects a clear imbalance in institutional demand, institutions are overwhelmingly favoring Bitcoin.

This preference is not just about performance, it’s about risk appetite and regulatory clarity. Bitcoin is perceived as a safer and more neutral asset: it has no founder risk, no central entity, and has stood the test of time. Most alts, on the other hand, carry high uncertainty since they're often backed by identifiable teams or venture capital, and many are seen as easily replaceable. Ultimately, this institutional dominance means that the consistent rallying asset has been Bitcoin alone. Without a wave of enthusiastic retail participation to push altcoins en masse, this cycle lacks the explosive “altseason” characteristics that defined previous bullruns.

What Can We Learn From This Cycle?

One of the biggest lessons from this cycle is that building a crypto portfolio is like setting up a football formation. You need the right mix of offense and defense—because as they say, offense wins games, but defense wins championships. Many investors came in hoping for fast gains, only to realize that resilience matters more than hype.

Unlike previous cycles, "this time is different" isn’t just a meme—it’s true. The dynamics have shifted. Institutional capital is leading the charge, market liquidity is fragmented, and capital rotates faster than ever between narratives. In this kind of environment, having 80% or more in Bitcoin isn't optional—it’s necessary. It’s the most reliable asset in the space, and the only one consistently rewarded in an institutional-driven market.

If you're still interested in altcoins, then understand this: you can’t just buy and hold anymore. With liquidity constantly rotating, the edge now lies in narrative timing and precision. And if you're diving into any trend, cherry-pick only those with strong utility and clear long-term value—because in a market flooded with tokens, most projects are replaceable.

In short, survival this cycle didn’t come from catching the wildest pumps—but from playing smart, defensive, and adaptable. The next cycle may look different again, but the principles of thoughtful allocation and strategic timing will never go out of style.