The Memory Misread

Written by Yohandi

SK Hynix is adjusting its mass production pace of HBM4, placing greater emphasis on the conventional DRAM market. The move reflects a resource allocation shift towards capturing additional profits in standard DRAM rather than engaging in an aggressive AI capacity race in HBM, where the company is in a dominant position with HBM accounting for more than 40% of revenue.

The official also stated:

Production forecasts for Nvidia’s next-generation chip Rubin (equipped with HBM4) are trending downward.

SK Hynix just made its own choice visible. Easing their HBM4 ramp pace so that they can harvest higher-margin commodity DRAM.

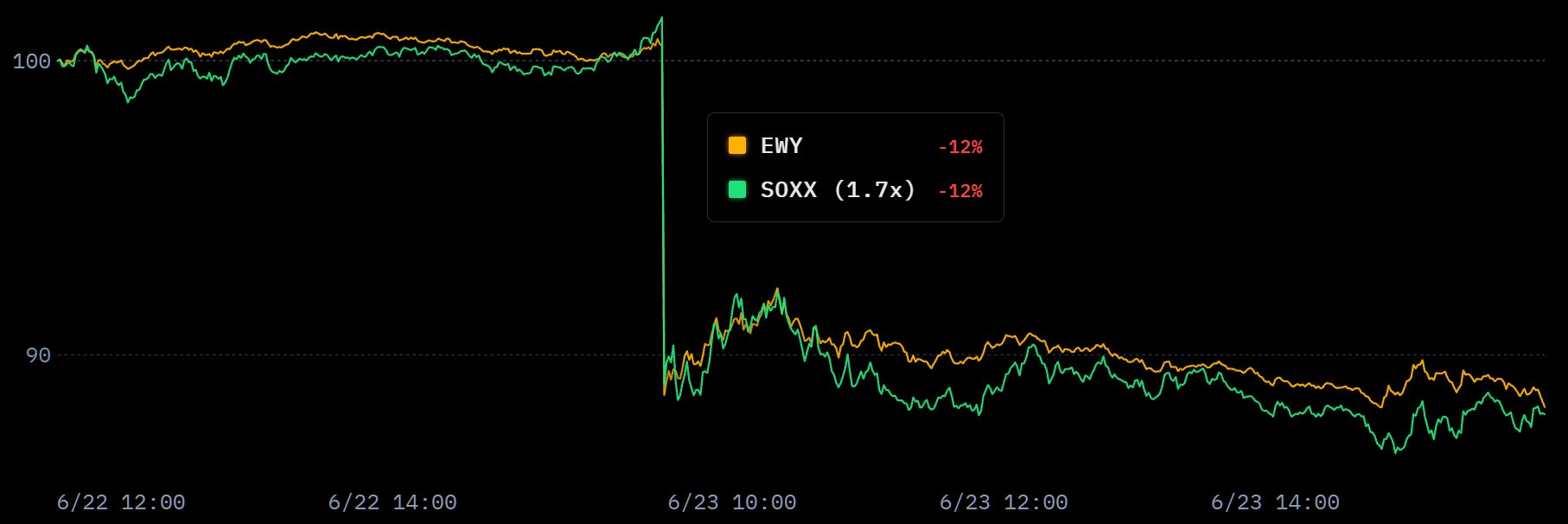

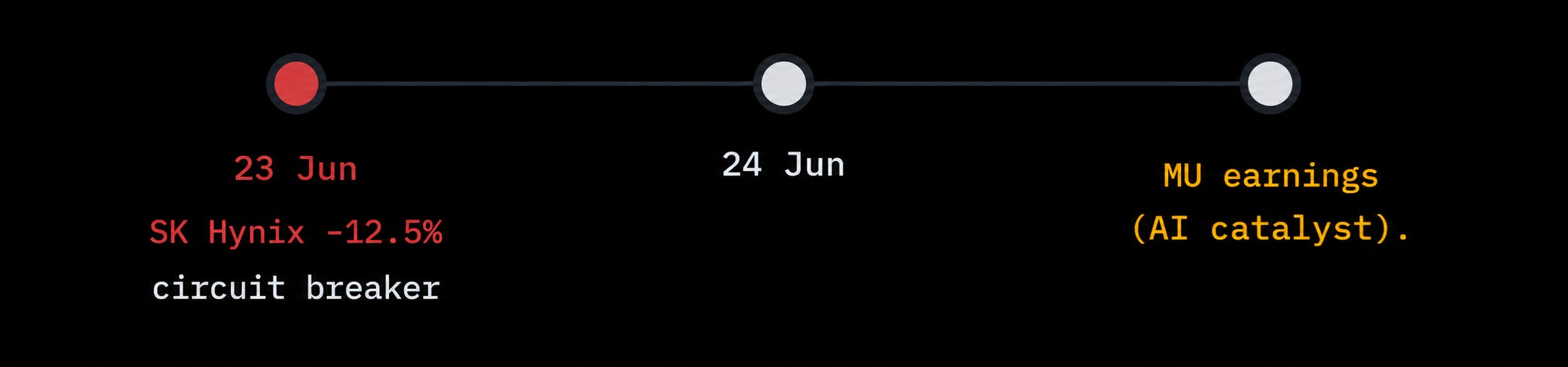

Compare the move of SOXX alongside EWY during the last two days. The selloff happening lately was actually pricing in towards the narrative of AI demand, specifically on memory industry. It is natural to worry that Micron will follow.

Why does this matter?

The three points implied from market:

HBM exists only to feed AI accelerators, so HBM orders are a clean proxy for AI demand.

HBM leader is easing its HBM4 ramp and supposedly would not slow its most strategic product unless it sees the demand behind it softening.

HBM leader is signaling a peak and the other two will follow, so the whole memory complex de-rates.

This writing can be your pre-earnings guideline for the upcoming Micron and a (presumably better) read on the “AI demand is cooling” scare in the semis complex.

What did SK Hynix actually do?

With its HBM revenue share already above 40% and a commanding lead established, SK Hynix is reportedly delaying the conversion of some HBM3E lines (which were scheduled to move towards HBM4) in order to capture more of the supply-constrained commodity DRAM market.

The trigger is easily seen as a profitability reversal. As of Q1 2026, the per-gigabit price of DRAM was still trailing HBM. But now the operating-margin gap has widened to more than 15pp in DRAM’s favor with one Korean brokerage arguing commodity DRAM operating margins could approach a theoretical 90% within the year.

Market’s current read:

The HBM leader is pulling back, so AI memory must be peaking.

A part that the market skipped: the downward Rubin forecast is a schedule (technical) effect that came from power, cooling, and interconnect validation pushing volumes out. So we can easily reject the cut-demand suspect; Blackwell, in fact, remains in heavy and profitable production in the meantime.

If we deconstruct this properly, Hynix’s tilt is more of a supply reshuffle. They schedule a change in capacity with a dominant share already secured towards a product paying the most today. Morgan Stanley made the same point from the top down, pointing to the memory-wide pricing cycle rather than HBM-share defense as the driver of value. They lifted SK Hynix estimates on a forecast that DRAM ASP rises ~62% in 2026.

HBM and DRAM lift each other

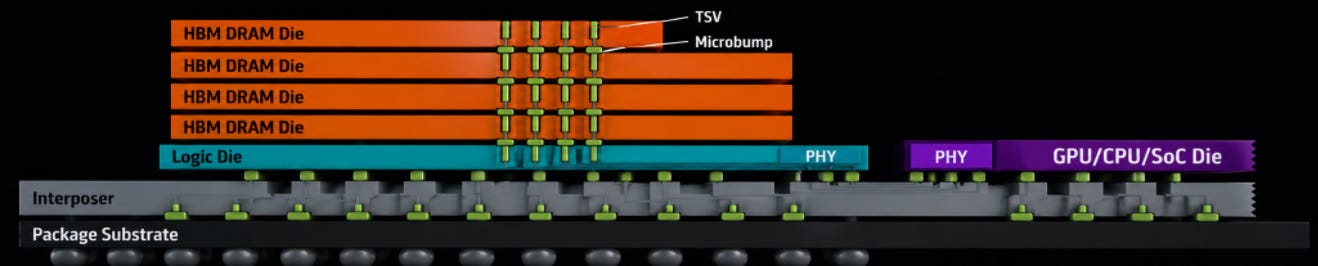

Pre-requisite: you should first understand how HBM is actually produced.

HBM is DRAM stacked with through-silicon vias and advanced packaging. It consumes about three times the wafers per bit of DDR5 (Micron). In simple terms, each unit of HBM built removes roughly three units of potential DRAM from supply. This drove DRAM into shortage. The squeeze lands on standard and PC memory, roughly 60–70% of the DRAM market — whose share is being ground down as wafers divert to AI. PC memory alone went from ~12% to ~9%.

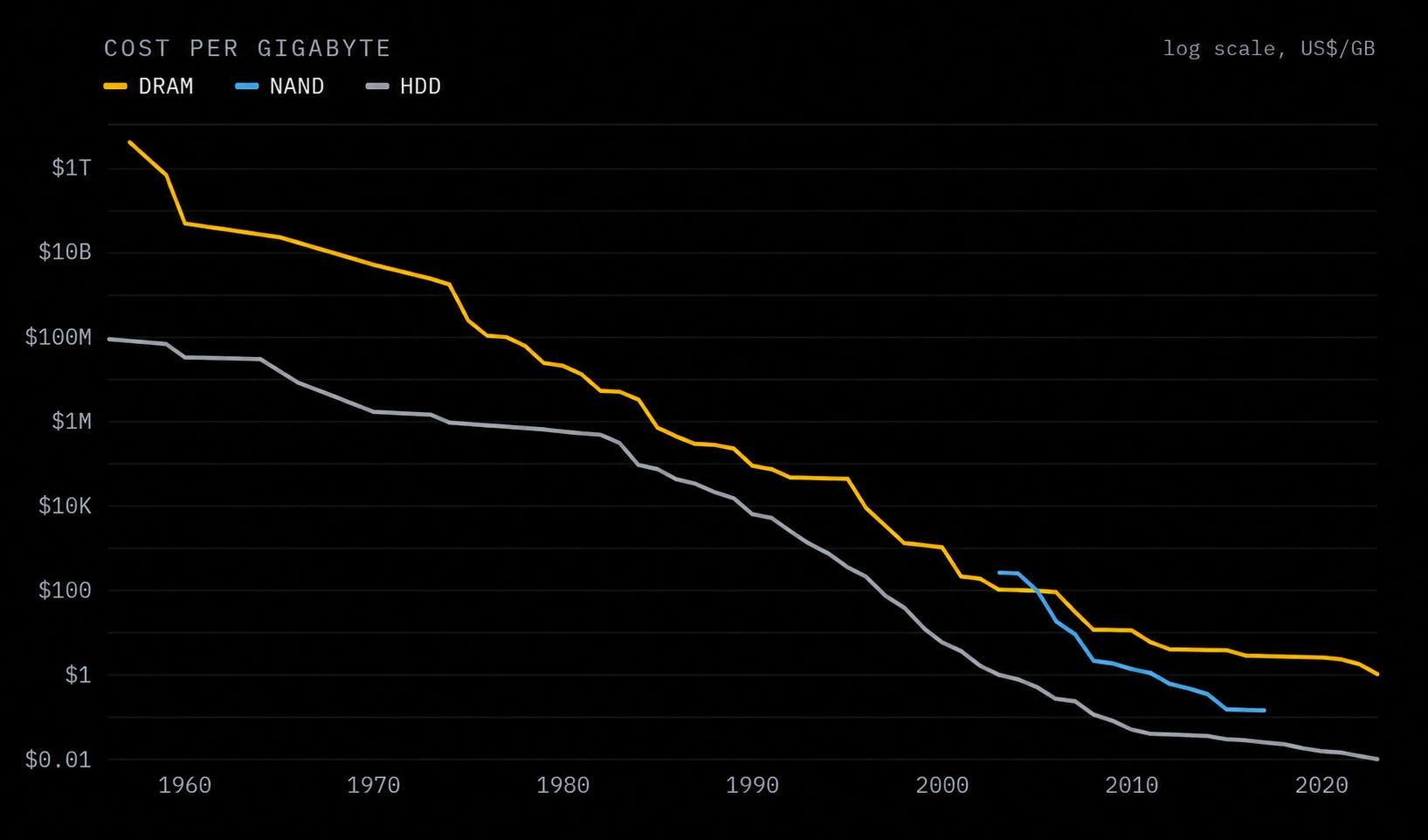

From the late 1950s to 2020, DRAM cost per gigabit fell by about an order of magnitude every five years (Moore’s Law in action). AI demand has now overturned that decades-long decline. A structural break.

With wafers concentrated on HBM and server DRAM, consumer prices spiked in 2Q LPDDR5X up 89% and LPDDR4X up 75% QoQ. Korea’s June export unit price for DRAM also ran up ~576% YoY (TrendForce), with overall memory exports on track for a record $38–42bn month as HBM (MCP) export value jumped ~51% in a single month. A demand story.

I believe the reason DRAM now shows a fatter margin is due to pricing structure. Not relative demand. HBM sells under multi-year agreements at locked prices, held stable through annual contracts even as the supply-demand imbalance stays severe. DRAM reprices frequently on the spot market. So in a shortage, it climbs in real time while the contracted product sits fixed at last year’s level, which is exactly how the >15pp margin gap opened up. Samsung said as much directly, conceding conventional DRAM is more profitable today. A conclusion that is the opposite of the bear read.

Important point: they are two outlets for one constrained wafer pool (not substitutes fighting over one customer). They are also in a strong-demand regime, so they hold each other up.

The 3:1 wafer draw starves the supply, so the HBM build is the direct cause of DRAM’s price surge. And when ordinary DRAM pays this well, the opportunity cost of dedicating a wafer to HBM rises (setting a higher floor under HBM pricing in the next round of contracts).

The makers will not sign cheap HBM when the alternative use of the same wafer is a booming spot market. So yes: HBM tightness lifts DRAM, and rich DRAM lifts HBM.

Hynix slowing HBM4 actually supports HBM pricing by restraining future HBM supply.

What should Micron be doing?

HBM’s base wafers are ordinary DRAM on a shared node. The industry measures HBM capacity by the TSV/packaging step that turns DRAM wafers into HBM wafers. Wafer starts can be allocated by margin. So, the front end is fungible.

To make DRAM instead of HBM, you just... don’t stack. (And you can sell it with higher margin now.) The only cost is opportunity cost plus the contractual obligation. So stepping back is cheap.

The hard floor is HBM is owed under LTA. Micron’s entire 2026 HBM output is committed under multi-year contracts that must be delivered; allocatable capacity is therefore everything excluding that floor.

Advanced packaging lines run at capacity and aren’t interchangeable with DRAM lines. By default, any front-end wafer that packaging can’t absorb as HBM flows to DRAM. Packaging caps HBM.

CSPs have reportedly booked essentially all of 2027’s contracted capacity and are already negotiating 2028, with the industry treating the 2027 shortage as worse than 2026. Makers are confident of further contract-price gains for two to three years. Micron can tilt toward DRAM, and doing so is rational.

The term “sold out” was also mentioned during Micron’s last guidance. One might think it describes the allocation; what I believe they meant was more toward the demand side. Using the fact that Micron’s fabs are flexible enough, the supply side can always be steered.

In light of the above, Micron can easily pivot. Should they?

Given that DRAM and HBM are reinforcing each other rather than cannibalizing, Micron does not need to abandon HBM to benefit from DRAM upside. The rational message is simply: higher ASP, richer margins, and disciplined value-based allocation, with HBM held as the strategic anchor and strong DRAM treated as upside. Product-agnostic margin guidance.

What it will not do is mirror Hynix’s HBM throttle, that move is rational for Hynix but largely unavailable to Micron. Micron’s position blocks the “throttling HBM” play while handing it the “capturing DRAM upside” for free. Supporting ideas: DDR5 out-earns locked HBM by >15 margin points, and Micron is already ~79% DRAM by revenue mechanically riding it up.

Which company is wrong? None of them.

Both firms converge on the same outcome: abusing fatter margins across a tight DRAM-plus-HBM complex. Just from opposite positions. The equilibrium is still self-reinforcing, high-margin oligopoly , & conditioned on demand staying strong.

What does it mean for the memory industry?

If I were to note the contemporaneous list of why the KOSPI fell, they are almost entirely technical:

Stretched leverage in Korean retail trading

A proposed tax on unrealized stock gains

Korea missing MSCI developed-market inclusion

Notice that none of those relate to a memory demand data point. Layer on the misread of Hynix’s tilt and Rubin’s technical delay.

The strongest discredit also comes from the demand side itself. NVIDIA’s Jensen Huang confirmed that all three makers (SK Hynix, Samsung, and Micron) are in production and fully supporting Vera Rubin. This pushed back on talk of sharp memory cuts, implying that future systems will still consume a great deal of high-speed memory. Even the largest buyer says demand is intact. Independent supply-chain checks agree. Rubin allocation is described as cutthroat and AI compute as supply-constrained at least through 2027, with steep premiums paid to lock capacity.

TL;DR

Bullish memory complex.

Future Work

Analyze whether memory-led hardware inflation becomes a fiscal or political risk, and whether supernormal margins in DRAM/HBM invite policy intervention.